CGAN-LSTM: Synthesizing the Volatile Pulse of Cryptocurrency Markets

The paper introduces a Conditional Generative Adversarial Network (CGAN) framework to generate high-fidelity synthetic cryptocurrency price time series. By combining an LSTM-based recurrent generator with an MLP discriminator, the model achieves state-of-the-art statistical consistency (Pearson correlation up to 1.0000) for Bitcoin, Ethereum, and XRP across high-volatility periods.

TL;DR

Researchers have developed a high-precision synthetic data generator specifically for the chaotic world of cryptocurrencies. By leveraging a Conditional Generative Adversarial Network (CGAN) with an LSTM backbone, the system reproduces minute-by-minute price movements of BTC, ETH, and XRP with near-perfect statistical correlation (). This provides a "privacy-safe" sandbox for testing financial AI without exposing sensitive institutional data.

Background: The Privacy-Utility Tradeoff in Finance

In the digital financial ecosystem, data is the new oil, but it is often locked behind "iron curtains" of regulation (GDPR, Open Finance) and strategic secrecy. For tasks like Money Laundering Detection or Volatility Risk Analysis, researchers need massive datasets that reflect real-world "black swan" events.

The authors position this work as a bridge: using Generative AI to create a "digital twin" of market behavior. Unlike simple mathematical models, this GAN-based approach captures the Inductive Bias of temporal sequences, allowing it to simulate the specific "panic" and "recovery" phases seen during the Russia-Ukraine conflict and major US monetary policy shifts.

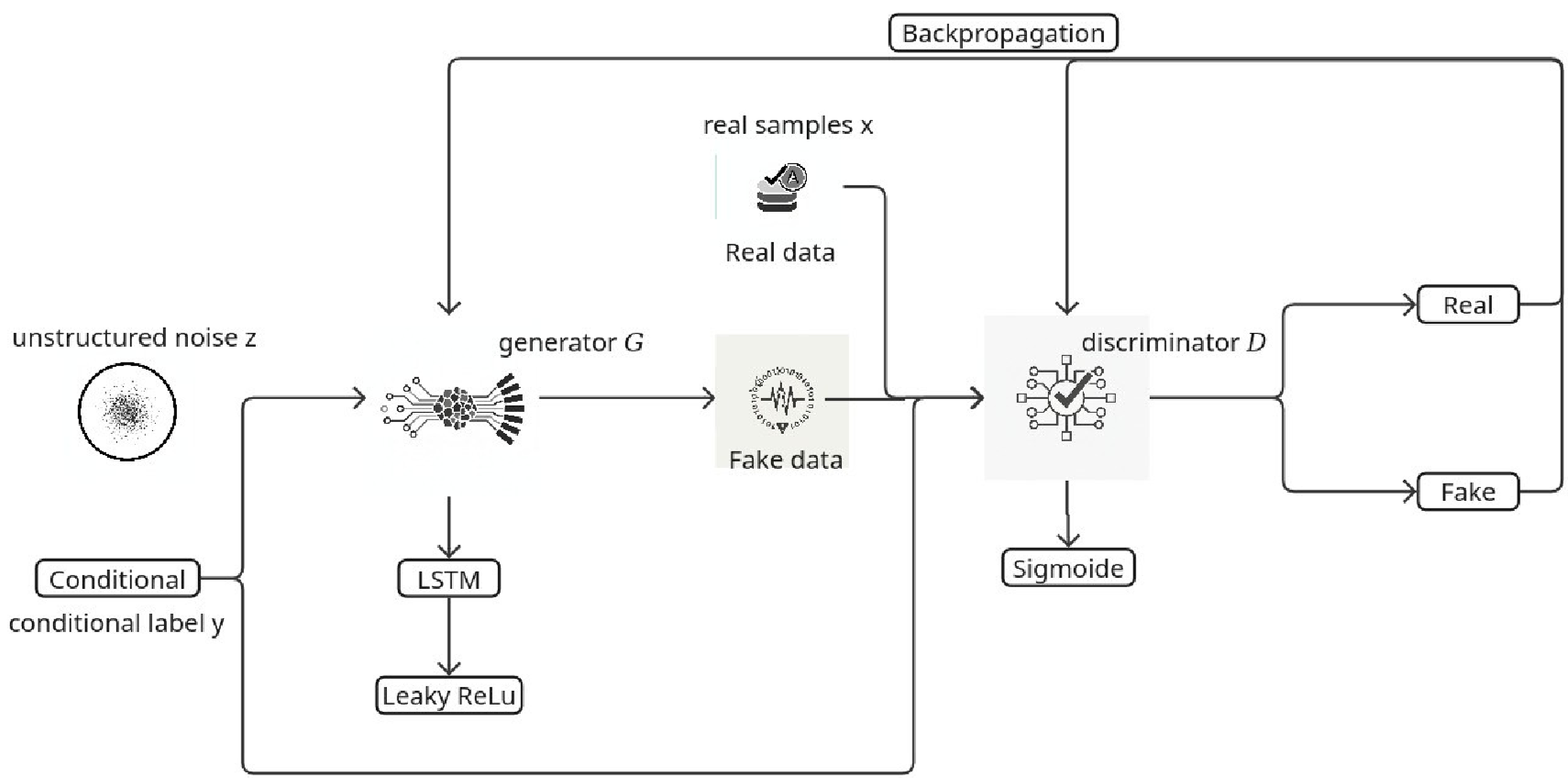

Methodology: The Architecture of Competition

The core innovation lies in the hybrid coupling of two distinct neural architectures:

- The Generator (LSTM): Chosen for its ability to maintain "Long Short-Term Memory." It takes a noise vector and a "condition" (the price at ) to predict the price at .

- The Discriminator (MLP): A Multilayer Perceptron that acts as a high-stakes critic, attempting to distinguish between the "Real" market data and the "Fake" synthetic prices.

Architectural Flow

The process utilizes BCEWithLogitsLoss for numerical stability, ensuring that gradients don't "explode" during the adversarial training—a common pitfall in financial GANs.

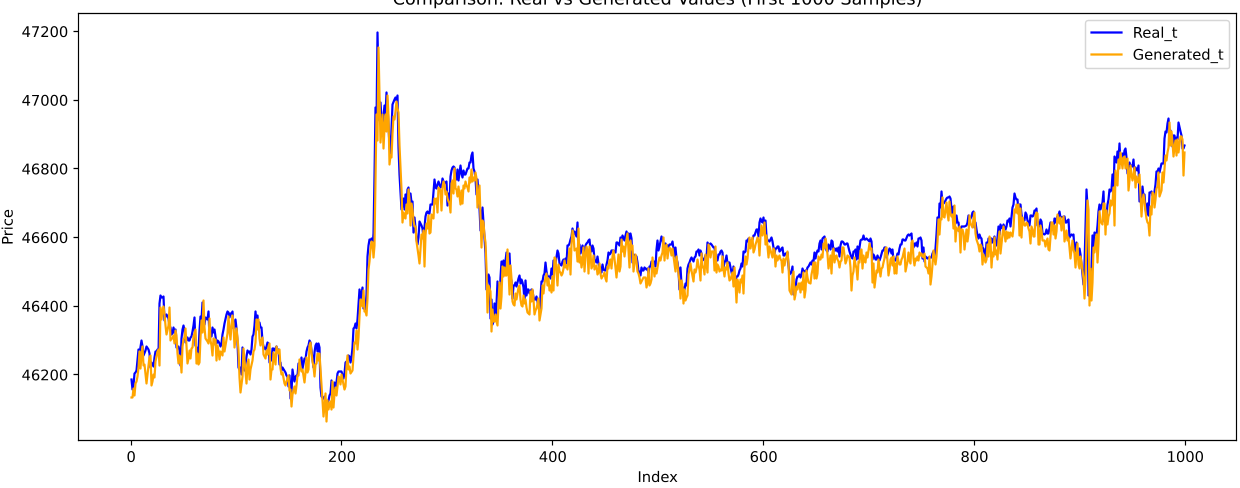

Experimental Results: Precision under Pressure

The model was tested across three "Volatility Scenarios" (VS), including the 2022 market crashes and projected 2025 trade shifts.

- Bitcoin (BTC): Showed the highest agreement. Its high liquidity makes it more "predictable" for the LSTM to learn.

- Ethereum (ETH): The model captured the trend but slightly "smoothed out" the most extreme volatility spikes, a known limitation where GANs struggle with heavy-tailed distributions.

- Quantifiably Accurate: The Pearson correlation scores reached 1.0000 in some sequences, meaning the synthetic data is statistically indistinguishable from real market movements.

Figure: The synthetic data (at 1000 samples) mimics the micro-fluctuations of the real BTC market with startling precision.

Figure: The synthetic data (at 1000 samples) mimics the micro-fluctuations of the real BTC market with startling precision.

Critical Analysis & Conclusion

Why it works

The effectiveness of this approach stems from the StandardScaler normalization and the 60-minute lookback window. By centering the data around a zero mean and unit variance, the authors mitigated the "gradient vanishing" problem that usually plagues RNNs.

Limitations

- Smoothing Effect: As seen in ETH and XRP results, the generator acts as a low-pass filter, occasionally failing to capture the absolute "climax" of a flash crash.

- Exogenous Blindness: The model relies purely on price history (). It cannot "see" a regulatory tweet or a protocol hack unless it is already reflected in the price.

Future Outlook

This research simplifies the path toward Stress Testing financial systems. Instead of waiting for the next market crash to test a trading bot, developers can now generate infinite "synthetic crashes" that follow the true statistical laws of crypto-volatility.